Small Change Making a Big Difference

This website may earn commissions from purchases made through links in this post.

Big goals can be both daunting and overwhelming.

We know what the end goal is, and we know what we need to do to get there…but it’s so far off in the distance that goal seems practically unattainable.

Take paying off the mortgage. 30 years is a loooong time to be paying off a debt.

But little by little we get there with two four key ingredients:

- Small steps

- Consistency

- Time

- Compounding

The Power of Compounding

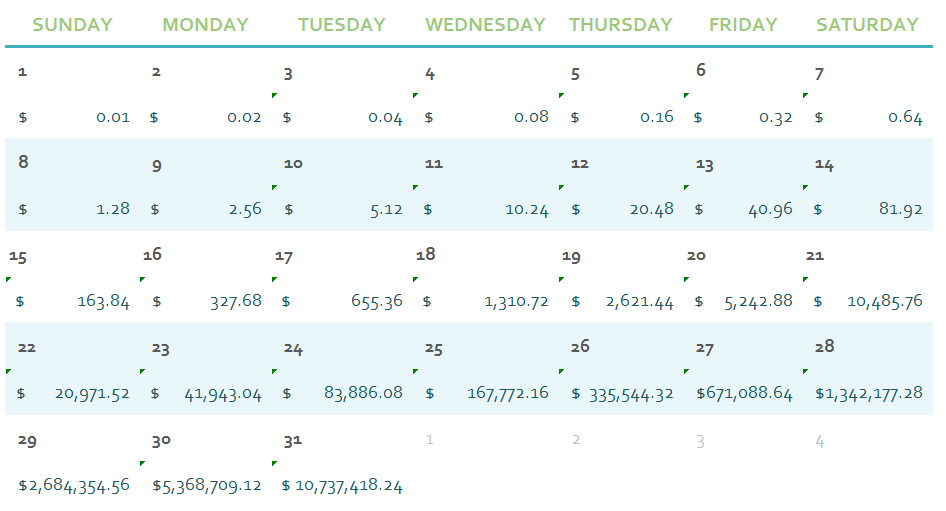

This question is an oldie but a goodie: Which would you take: $1 million dollars straight in the hand OR 1 cent, doubled every day for a month?

You know this is a trick question, so you’ll probably take the 1 cent, which would be the correct answer.

In fact, you could beat that million dollars tenfold, assuming you picked the right month (not February!).

Here’s how the maths unfolds:

Yeah, I know, back in the real world, we’re never going to find an investment that doubles our money every day.

But what this example does show is how compounding works and how it’s important to ‘run the numbers‘ not just make a decision based on face value.

Take a look at the first few weeks. Not much happening there, folks. Nothing to see.

That’s why it can feel like you’re getting nowhere when you’re taking small steps towards your financial goals.

But then, halfway through the month, things start to really gain momentum. The power of compounding kicks in.

And by the end of the month, our 1 cent investment has outstripped the $1 ten million times over.

But you need all the players: small change, time, consistency and compounding to see the result.

How one soft drink can save you $30,000

Let’s say you have a $3 a day soft drink habit (weekdays only) that you want to redirect to your mortgage. Before I get into the maths of how this seemingly small amount can save you a packet of money, let’s look at a variation of the compounding effect of not drinking that soft drink each day.

A can of cola beverage (insert your favourite trademarked beverage here), is about 138 calories. 1 can less a day gives you a 2,760 calorie deficit each month.

Over the course of a year, wait for it, you consume 33,120 calories less by cutting out just one can of soft drink a day.

Small changes make a big difference.

In financial terms, that adds up to not spending $720 a year.

Now let’s see what happens if you were to put this $3 to your mortgage instead of just saving it.

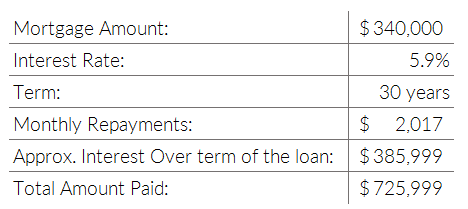

Just say you have a mortgage that looks something like this:

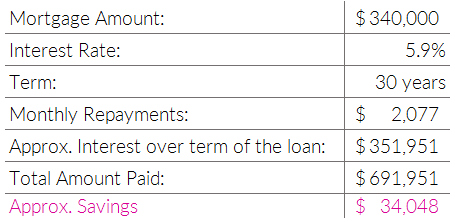

Now here’s the effect of paying an extra $60 per month ($3 x 5 days x 4 weeks) assuming all things equal and interest doesn’t fluctuate etc. (it’s never like that in real life, but we’ll assume it here for the sake of the maths):

It’s not $10 million dollars, but it’s still pretty impressive for one small change.

From little things, big things grow as they say, or small changes make a big difference. What small change are you going to make today?

Any amount, no matter how small, does add up in the end. This year I challenged myself to be able to save money by cutting down green tea latte ( this is my vice, I know the others love coffee) and so far so good! I am looking forward to attaining my goal of purchasing my very first car. :)

Good on you and good luck!

Yes it is true. If I can continue on this new track I will be mortage free in less than 7 years. Which is good as Im 56 years old, with hardly any super. However as I am blessed to have full time work at moment, Im making the most of it. Visitng this site is my Friday treat.

Home alone, no heating on, layers of clothes ,hotwater bottle and one lampon. Not miserable but empowered. I am saving!! You have helped with my change of mind. Frugal and thriving. Thanks.

Good luck Sue! That’s very inspiring. It’s all about mindshift :). I love snuggling with a hot water bottle. Such a delicious comfort on a cold night.

Indeed little drops can make an Ocean.

Thanks for this beautiful article.

Lovely content and a beautifully written article.

Mel, I love your saving 1 cent a day, doubled every day for a month – excepting, in these high-inflation times, we no longer have 1 or 2 cent coins, so it’s 5 cents – which will make you FIVE TIMES richer at the end of those 30 days, so a classic case of win-win-win-win-win (5x win)…!

May I second Rob Wilson’s comment, and say I entirely agree with what he wrote. You are a gem, Mel! As a long-time lurker on this site, I often return for a wee browse, and I always find something you wrote to inspire me.

May you go on writing these useful articles and essays for a very long time – and ditto me going on reading your most excellent site…

Thanks JDW :)